Alternative to Traditional Equities

RBIs provide highly efficient access to frequently rebalanced long-equity strategies. Clients may use these notes to participate in international equity markets and sectors, thereby diversifying their equity holdings. Other asset classes, such as fixed income, can be applied to these notes and are dynamically accessed. This is beneficial to clients wanting to vary their participation in both the equity and bond markets during unstable market conditions. Currency hedges are also offered on a variety of notes. These hedges are best for clients wanting global exposure to equity markets, but want to reduce the uncertainty of currency fluctuations.

Systematic Investing

Because these securities are rules-based, the emotional aspect of investing is removed. The Securities follow the pre-defined strategy throughout their term, and market exposure is either increased or decreased depending on the rules of the strategy.

Customizable Products

The strategies are typically designed by RBC Research but can also be customized to reflect individual investment views. For example, an advisor and/or client may choose the initial portfolio of shares, the strategy that governs future share selection, and whether a currency hedge is required.

Operationally Efficient

RBIs are efficient because they offer a “one-ticket solution”. RBC teams trade the underlying shares and rebalance each portfolio. All costs to investors are reflected in the annual fee. RBC offers a daily secondary market for clients wishing to redeem positions prior to maturity.

- These notes are not principal protected.

- Investors may lose all or part of their principal invested in the securities.

- Strategies are pre-defined and cannot be changed during the term of the note. RBI investors can sell an RBI in the secondary market if their investment view has changed.

How it works

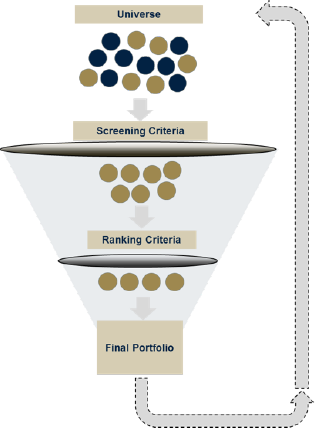

Choosing a StrategyStrategies tend to follow a standard set of steps:

- Universe: A universe of stocks, such as the S&P/TSX Composite Index, the S&P500 Index etc. is first pre-defined.

- Screening Criteria: Stocks are screened from the universe based on pre-selected factors, reflecting the investment theme. For example, a “value” investment theme would screen for low P/E and low P/B ratios, whereas an “income” theme would screen stocks using dividend yield, dividend payout ratios etc.

- Ranking Criteria: Highly ranked stocks are then filtered into the portfolio and held for a pre-defined period, such as a month or a quarter.

- Portfolio Re-balancing: The portfolio is reviewed at set intervals and stocks that no longer meet the above criteria are replaced with new stocks that do.

This process is akin to the role of a Portfolio Manager, with the added benefit that the resulting strategy is not subject to emotional biases or style shifts due to manager turnover.

Click here to see examples of currently offered Rules-Based Strategies.

Tactical overlays can be used on the equity portfolio to reduce risk when market conditions warrant. The percentage allocation is adjusted based on pre-defined rules. Tactical overlays can vary across asset classes from, fixed income to commodities to defensive stock portfolios.

While strategies that employ tactical overlays do not claim to time the market, they have the potential to increase or reduce market exposure when certain market indicators are triggered. Typically, it would be up to an investor to vary equity exposure - however, with a tactical overlay, once an event is triggered, the strategy would automatically invest in the alternate asset.

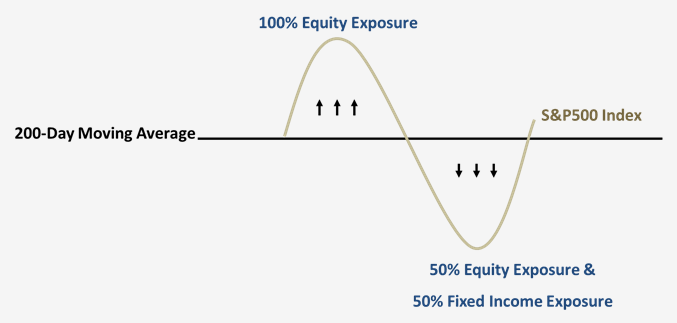

A common market indicator is the 200-Day Moving Average (200DMA). A tactical strategy could use the 200DMA indicator to achieve the desired market exposure. Usually, when an index trades above its 200DMA, investors view this as a sign of positive market sentiment. For example, as demonstrated in the chart to the right, in this strategy when the index is above the 200DMA, the equity portfolio is 100% exposed to the equity investment.

When the index trades below its 200DMA, it is a negative signal. The chart on the right shows that the portfolio will move to a more defensive allocation, in this case 50% Equity / 50% Fixed Income.

Click here to see examples of Tactical strategies.